Energy Wholesale Market Review

Energy Wholesale Market Review Week Ending 25th January 2019

All wholesale power and gas contracts fell this week. Prices have been pressured towards the end of the week by forecasts of warmer temperatures over the weekend, falling commodity prices and a well-supplied gas system. All baseload power contracts fell, with day-ahead power down 7.5% to end the week at £59.5/MWh, weighed on by falling gas and commodity prices. Seasonal power contracts were down 2.4% on average. All gas contracts fell as temperatures lifted towards the end of the week and the gas system was well supplied with an increase in LNG imports. Day-ahead gas decreased 7.7% to 57.7p/th, although forecasts of below seasonal temperatures from 28 January could lift prices this week. Seasonal gas contracts slid 5.6% on average. Summer 19 gas fell 9.2% to a seven-month low of 50.2p/th. Brent crude oil prices were up 1.8% to average $61.7/bl. Prices dropped in the middle of the week following reports that US crude stocks rose to 445mn barrels. However, Brent crude prices recovered after the US threatened to impose sanctions on crude exports from Venezuela. API 2 coal prices rose 1.7% to average $86.0/t. Coal prices dipped towards the end of the week to $85.7/t as an uptick in temperatures in continental Europe lowered demand. EU ETS carbon prices were up 5.7% to average €24.5/t. Carbon prices found support last week as below seasonal normal temperatures across Europe pushed up power demand and led to an increase in conventional power generation amid a period of low wind generation.

Energy Wholesale Market Review Week Ending 25th January 2018

Energy Wholesale Market Review Week Ending 18th January 2019

All wholesale power and gas contracts rose this week. Prices have been supported by the recovery of commodity prices, below seasonal normal temperatures and tighter supply margins amid nuclear outages and weaker wind generation. With half of UK nuclear capacity offline due to planned and unplanned outages this week, day-ahead baseload power was up 3.1% from the previous week to £64.4/MWh. All seasonal baseload power contracts went up week-on-week, rising 3.8% on average. Gas contracts also rose this week, with day-ahead gas up 5.4% to 62.5p/th, as gas for heating demand went up towards the end of the week following much colder temperatures. February and March 19 gas climbed 1.6% and 1.2% to 62.9p/th and 60.7p/th respectively. Seasonal gas contracts were up 2.7% on average, with summer 19 gas increasing 3.3% to 55.3p/th, following oil prices higher. Brent crude oil prices rose for the second consecutive week, up 1.2% to average $60.6/bl. Prices have risen as data showed OPEC’s production cuts coming into effect, despite news that US crude production hit a record 11.9mn bpd the previous week, up from 11.7mn bpd the week before. EU ETS carbon prices recovered from last week’s decline, rising 3.8% to average €23.2/t. Within-day carbon prices reached a high of €24.7/t on 18 January, the highest since 3 January. API 2 coal prices went up for the first time in three weeks, increased 2.9% to average $84.6/t. Coal prices have been supported by colder temperatures across Europe, increasing demand for coal-fired power generation.

Energy Wholesale Market Review Week Ending 18th January 2018

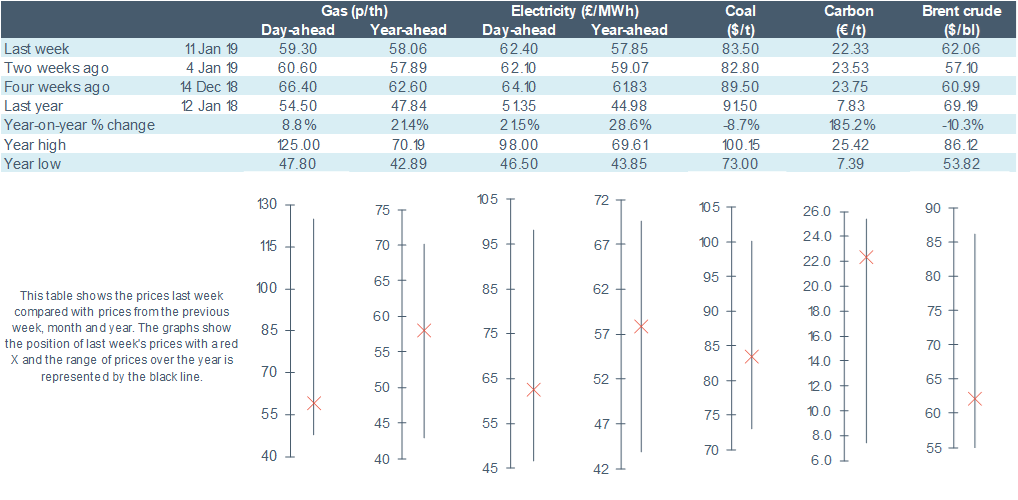

Energy Wholesale Market Review Week Ending 11th January 2019

Wholesale power and gas contracts experienced mixed movements this week, as most baseload power contracts and near-term (up to and including summer 19) gas contracts followed EU ETS carbon and API 2 coal prices lower, whilst recovering Brent crude oil prices pushed seasonal gas contracts up. Most baseload power contracts fell, with day-ahead, winter 20 and summer 21 the exceptions. Day-ahead power started the week at a one-month low of £57.0/MWh; however, forecasts of lower wind generation supported prices towards the end of the week, rising 0.5% to £62.4/MWh. Most seasonal baseload power contracts fell, down 0.7% on average. Near-term gas contracts up to and including summer 19 fell. Day-ahead gas was down 2.1% to 59.3p/th, as forecasts of milder temperatures until 18 January, and firm LNG send-out so far this year, have pressured prices. Day-ahead gas dropped to a five-month low of 57.0p/th on 10 January. Seasonal gas contracts rose 1.5% on average, however, summer 21 gas dropped 0.4% to 53.5p/th. Brent crude oil prices recovered from the previous week, rising 8.5% to average $59.8/bl as OPEC’s 1.2mn bpd production cut began. API 2 coal prices dropped 2.8% to average $82.2/t, pressured by a milder start to the year, full coal stocks and increasing competition from gas in European markets. EU ETS carbon prices dropped 9.7% to average €22.4/t. Weak demand at auctions led within-day carbon prices to drop to $21.4/t on 10 January, a one-month low.

Energy Wholesale Market Review Week Ending 11th January 2018

Energy Wholesale Market Review Week Ending 4th January 2019

Nearly all wholesale power and gas contracts fell week-on-week, with day-ahead peak power the exception, up 1.7% to £68.2/MWh. Day-ahead power fell 0.6% to end the week at £62.1/MWh, amid forecasts of higher wind generation early next week. The new month-ahead (February 19) power contract also dropped, ending the week at £63.9/MWh, whilst March 19 power decreased 1.6% to £61.2/MWh. All seasonal baseload power contracts fell week-on-week, down 3.0% on average. Summer and winter 19 were down 3.4% and 2.7% to £56.0/MWh and £62.1/MWh respectively, both four-week lows. All gas contracts decreased this week, with near-term contracts pressured by above seasonal normal weather at the start of the year. Week-on-week day-ahead gas fell 3.0% to 60.6p/th, 0.6% above the same time last month when it was 60.3p/th. Seasonal gas contracts were down 2.2% on average. Summer and winter 19 gas dropped 3.6% and 2.6% to 53.7p/th and 62.1p/th respectively. Brent crude oil prices slipped from an average of $55.2/bl the previous week to an average of $55.1/bl this week. Prices ended 2018 at $53.8/bl but rose above $57.0/bl by the end of the week as OPEC production cuts began on 1 January. API 2 coal prices dropped 2.6% to average $84.6/t. Coal prices ended the week at $82.6/t, the lowest since 19 April 2018. EU ETS carbon prices curtailed 1.5% to average €24.8/t, down from €25.2/t the previous week, despite there being no auctions scheduled until 7 January.

Energy Wholesale Market Review Week Ending 4th January 2018

Written By Graham Paul

{kind=link}