Energy Wholesale Market Review

Energy Wholesale Market Review Week Ending 22nd February 2019

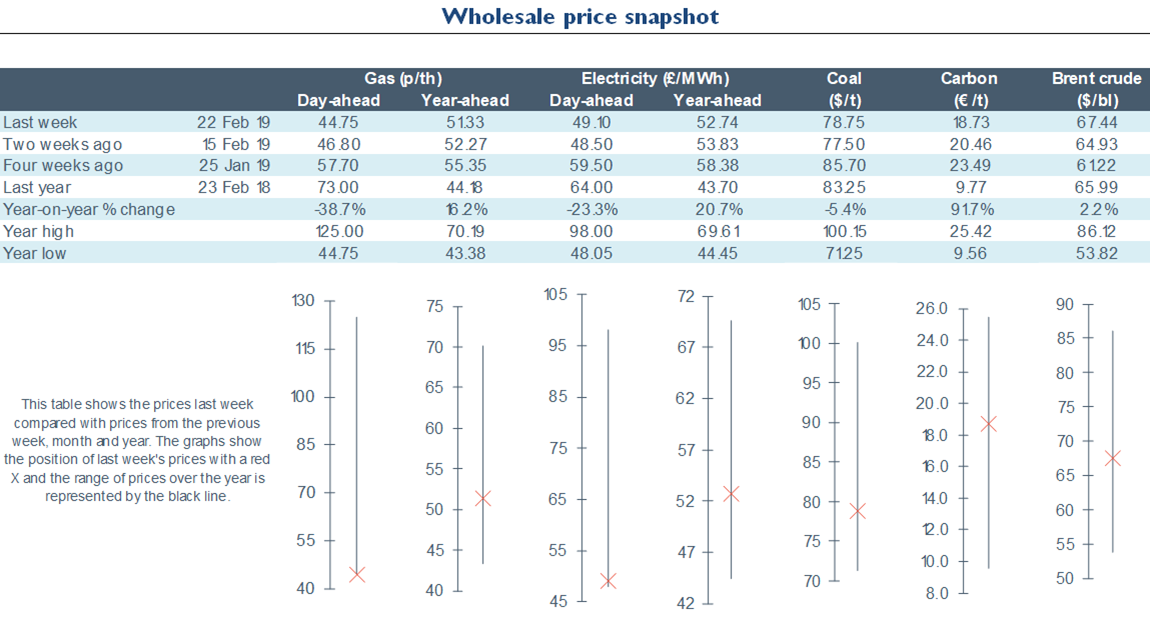

Nearly all wholesale gas and power contracts fell this week, with day-ahead power the only exception amid forecasts of lower wind generation next week. Wholesale prices have continued to be pressured by milder temperatures, lower demand and comfortable gas supplies, despite three-month high Brent crude oil prices. However, day-ahead power rose 1.2% to end the week at £49.1/MWh, amid forecasts of lower wind generation. The contract hit a fresh eight-month low of £48.1/MWh on 19 February as wind generation was forecast higher the following day. Seasonal power contracts decreased 1.5% on average from the previous week and were an average of 7.4% lower than the same time last month. All gas contracts continued lower this week. The gas system remained comfortably supplied, with the arrival of LNG tankers, milder temperatures, and strong supplies from Norway despite an outage at Aasta Hansteen gas field. Day-ahead gas dropped 4.4% to end the week at a fresh 17-month low of 44.8p/th. This is the lowest since 23 October 2017 and 28.3p/th below the same time last year. Brent crude oil rose for the third consecutive week, up 5.2% to average $66.7/bl. Within-day oil prices rose above $67.5/bl on 22 February, the highest since 16 November 2018. EU ETS carbon prices fell 5.1% to average €19.9/t. Within-day carbon prices fell below €18.5/t on 22 Friday, a fresh three-month low. API 2 coal prices started to reverse recent declines, up 2.6% to average $78.0/t.

Energy Wholesale Market Review Week Ending 22nd February 2019

Energy Wholesale Market Review Week Ending 15th February 2019

All wholesale gas and power contracts fell this week. Prices continue to be pressured by milder temperatures, lower demand and comfortable gas supplies. This fall was despite a recovery in Brent crude oil prices which went above $65/bl for the first time since November 2018. All baseload power contracts fell week-on-week, following their gas counterparts lower. Day-ahead power was down 9.8% to end the week at £48.5/MWh, a fresh eight-month low. Seasonal power contracts decreased 3.1% on average, with summer 19 power declining 4.7% to £49.2/MWh. The contract hit a fresh eight-month low of £48.8/MWh on 13 February. All gas contracts fell amid an oversupplied gas system following the arrival of several LNG tankers, comfortable flows from Norway and milder temperatures. Day-ahead gas dropped 5.0% to end the week at 46.8p/th, the lowest since 31 October 2017. Seasonal gas contracts fell 1.0% on average, as summer 19 gas fell 2.6% to 45.9p/th, a fresh nine-month low. Brent crude oil rose for the second consecutive week, gaining 1.8% to average $63.4/bl. Within-day oil prices rose above $65.0/bl on 15 February, the first time since 20 November 2018. EU ETS carbon prices fell 9.6% to average €21.0/t. Carbon prices have been pressured by weak EU economic data, whilst warmer temperatures and falling gas prices have reduced demand for buying EUAs. API 2 coal prices dropped 5.5% to average $76.0/t. API 2 coal prices dropped to a 21-month low of $71.3/t on 11 February, amid forecasts of warm temperatures for the rest of February in NW Europe.

Energy Wholesale Market Review Week Ending 15th February 2019

Energy Wholesale Market Review Week Ending 8th February 2019

All gas contracts fell this week, whilst power contracts experienced mixed movements. Prices were pressured by milder temperatures, lower demand and comfortable gas supplies this week. Day-ahead power dropped 1.4% to end the week at £53.8/MWh. The contract had fallen to an eight-month low of £50.8/MWh on 7 February as storm Erik was expected to increase peak wind output to 12GW the following day. March and April 19 power contracts rose 0.5% and 0.2% to £53.7/MWh and £52.8/MWh respectively. Seasonal power contracts lifted 0.1% on average from the previous week. However, summer 19 power slipped 0.4% to £51.6/MWh. All gas contracts fell as the gas system was well supplied following the arrival of several LNG tankers, comfortable flows from Norway and milder temperatures throughout the week. Day-ahead gas dropped 5.5% to end the week at 49.3p/th, a fresh 10-month low. March and April 19 gas also dropped, down 1.6% and 1.2% to 49.7p/th and 48.4p/th respectively. Seasonal gas contracts fell 1.6% on average, with summer 19 gas down 2.3% to end the week at 47.1p/th, a fresh seven-month low. Brent crude oil prices recovered from the previous week’s decline, up 1.7% to average $62.2/bl. Within-day oil prices rose to a two-month high of $63.6/bl on 4 February. API 2 coal ended the week at $77.65/t, a 10-month low, as the Chinese New Year holiday saw a hiatus in trading and lower demand in the region. EU ETS carbon was up 2.5% to average €23.2/t, having dropped to a two-month low of €21.3/t on 4 February.

Energy Wholesale Market Review Week Ending 8th February 2019

Energy Wholesale Market Review Week Ending 1st February 2019

All wholesale power contracts and most gas contracts fell this week. Prices were pressured by forecasts of nearer seasonal normal temperatures in February, easing demand, comfortable gas supply margins, and falling commodity prices. All baseload power contracts fell week-on-week. Day-ahead power dropped 8.4% to a seven-month low of £54.5/MWh, following its gas counterpart lower. Seasonal power contracts fell 3.3% on average from the previous week, with summer 19 power down 5.6% to £51.8/MWh, the lowest since August 2018. Most gas contracts fell as the gas system was well supplied amid increased LNG imports, high storage levels and forecasts of milder temperatures. Day-ahead gas dropped 9.7% to 52.1p/th, a nine-month low and 0.1p/th above the same time last year when the contract was 52.0p/th. Although most seasonal gas contracts rose, a 4.0% week-on-week drop in the summer 19 gas contract saw seasonal gas prices down 0.6% on average. Summer 19 gas started February at 48.2p/th, the lowest since 21 June 2018. Brent crude oil prices fell for the first time in five weeks, down 0.8% to average $61.2/bl as economic data shows slower than expected growth in China, signalling weaker demand for oil. API 2 coal prices slipped 1.4%, reversing the previous week’s gains and averaging $84.8/t. Coal prices have fallen amid forecasts of milder temperatures in February across Europe and weaker coal demand in Asia. EU ETS carbon prices dropped for the first time in three weeks, down 7.9% to average €22.6/t.

Energy Wholesale Market Review Week Ending 1st February 2019

Written By Graham Paul

{kind=link}