Energy Wholesale Market Review

Energy Wholesale Market Review Week Ending 27th August 2021

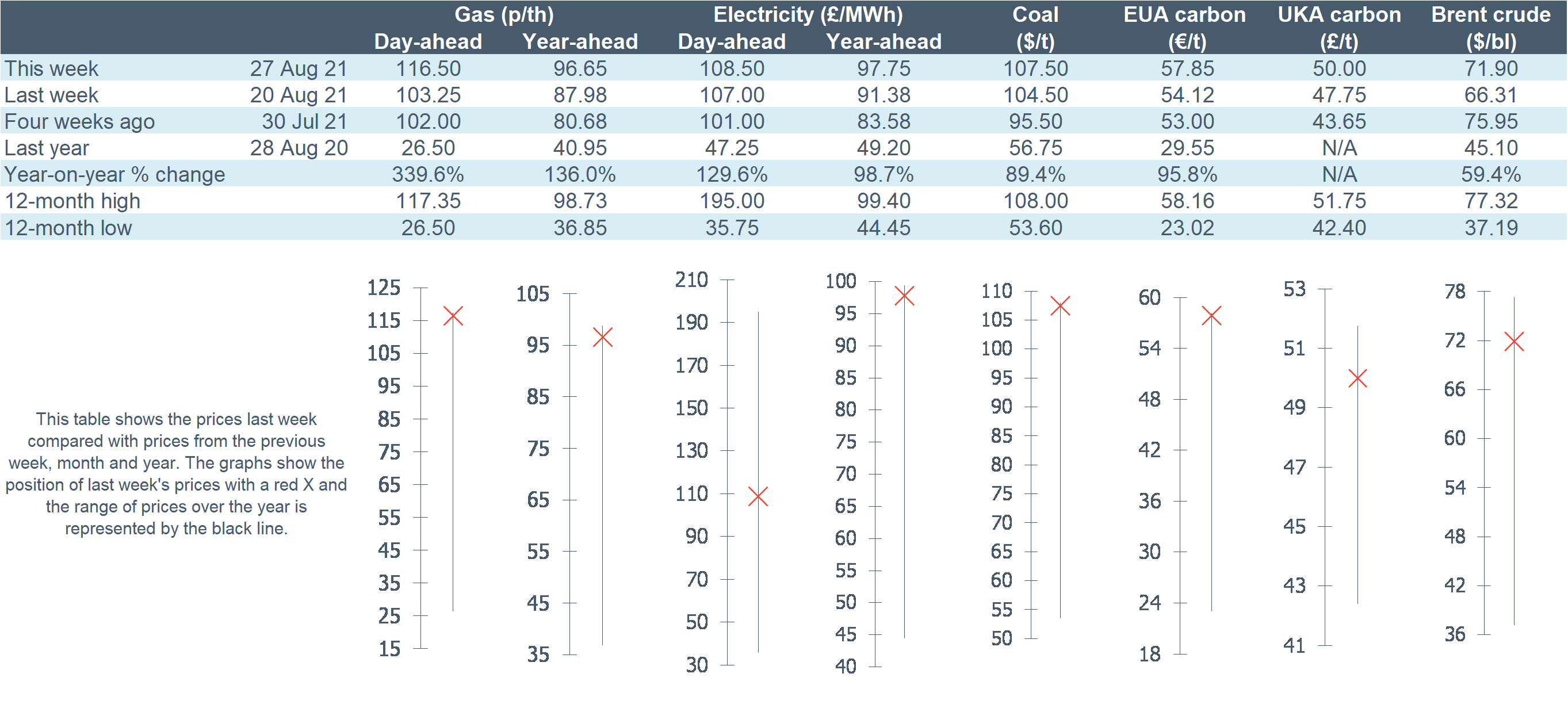

Bullish momentum across gas and power markets continued this week, following a short-lived bearish period of prices in the week prior. Subsequently, day-ahead gas rose 12.8% to 116.50p/th, following a stronger demand profile observed throughout the majority of the week, combined with lowering Norwegian gas flows, restricting gas supply into GB in turn. Day-ahead power mirrored the bullish trends observed in gas contracts, rising 1.4% to £108.5/MWh, taking direction from the gas market and higher demand in the week. September 21 gas was up 14.1% at 117.50p/th, and October 21 gas increased 11.8% to 118.50p/th. Seasonal gas contracts experienced similar upward movement, rising by 7.3% on average. This saw both winter 21 and summer 22 gas growing 12.7% and 5.4% respectively, lifting to 120.80p/th and 72.50p/th. All seasonal power contracts also grew, up 5.0% on average. Brent crude prices rebounded this weeks, with week-on-week prices rising for the first time in four weeks. As such, prices rose 2.7% to $70.13/bl. The UK ETS fell for the first time in nearly five weeks this week, subsequently falling 0.4% lower to £49.02/t. The EU ETS shared these losses, down 0.2% to €56.49/t.

Wholesale price snapshot

Energy Wholesale Market Review Week Ending 27th August 2021.

Energy Wholesale Market Review Week Ending 20th August 2021

On balance, the picture for gas and power prices this week was predominately mixed, but slightly favouring a more bearish outlook. Whilst a significant amount of contracts across gas and power markets fell this week, prices generally remain at significant highs, achieving record highs in the week also. Day-ahead gas fell 6.1% to 103.25p/th, in what transpired as a relatively volatile week for gas prices. Prices exceeded three-year highs across three separate days during the week, predominately buoyed by higher gas-for-power demand. Friday-on-Friday prices ultimately fell with the announcement from Gazprom that they could pump 5.6bcm of gas via Nord Stream 2, with flows expected by the end of this year. Day-ahead power rose 1.9% to £107/MWh, taking direction from bullish price movements on near-term gas contracts, particularly at the mid-points of the week. A three-year high was also achieved on 18 August at £128.00/MWh. September 21 gas was down 9.0% at 102.96p/th, and October 21 gas decreased 8.1% to 106.04p/th. Most seasonal gas contracts declined this week, down by 3.1% on average, while both winter 21 and summer 22 gas dropped 7.5% and 4.3% respectively, subsiding to 107.17p/th and 68.79p/th. The majority of seasonal power contracts fell this week, down on average by 2.2%, as winter 21 power decreased 5.1% to £107.50/MWh, while summer 22 fell 3.8% to £75.25/MWh.

Wholesale price snapshot

Energy Wholesale Market Review Week Ending 13th August 2021

The bullish picture for gas and power markets generally continued this week, with most contracts rising or holding onto recent gains. Subsequently, day-ahead gas rose 0.9% to 110.00p/th, supported by a back-drop of low gas in storage across Europe and the UK. Day-ahead power looking at Friday-on-Friday price movements, remained unchanged at £105/MWh, maintaining recent highs, continuing to take direction from record highs in near-term gas contracts. September 21 gas was up 1.8% at 113.18p/th, and October 21 gas increased 2.6% to 115.33p/th. All seasonal gas contracts grew this week, up by 5.1% on average, with both winter 21 and summer 22 gas rising 3.9% and 7.9% respectively, lifting to 115.91p/th and 71.89p/th. Most seasonal power contracts boosted this week, up on average by 3.5%, as winter 21 and summer 22 expanded 1.1% and 5.7% respectively, increasing to £113.25/MWh and £78.25/MWh. Brent crude oil slipped for the second consecutive week this week. As such, prices averaged 3.2% lower than the previous week at $70.19/bl. The most notable price set-backs were observed at the week’s start, driven by news of increased travel restrictions in China amid rising COVID-19 cases, fuelling demand recovery fears. Carbon markets rose for the third consecutive week, building on strong recorded gains. Subsequently the UK ETS rose 3.1% to £48.09/t, with the EU ETS sharing these bullish price movements, up 2.6% to €56.77/t.

Wholesale Price Snapshot

Energy Wholesale Market Review Week Ending 13th August 2021.

Energy Wholesale Market Review Week Ending 6th August 2021

Retaining their bullish momentum, the majority of gas and power contracts reported gains this week. Day-ahead gas rose 6.9% to 109.00p/th, finding support from lower UKCS production and a drop in Norwegian imports during the week, alongside forecasts of increased gas-for-power demand at the week’s end. Despite reducing mid-week, day-ahead gas prices reached a more-than three-year high on 2 August of 109.00p/th, rising back to this level on Friday. September 21 gas rose 8.8% to 111.15p/th, and October gas traded 7.6% higher at 112.42p/th. All seasonal gas contracts saw price rises this week, up by an average of 8.6%. Following its gas counterpart, day-ahead power went up 4.0% to £105.00/MWh, while also finding support on Friday from forecasts of weaker wind output at the start of next week. September 21 power increased 10.3% to £110.00/MWh and October 21 power elevated 2.8% to £104.50/MWh. Seasonal power contracts averaged an increase of 9.6% this week. Brent crude oil slipped marginally, down 3.2% to average $72.50/bl. Prices were weighed on news of the rising prevalence of the Delta variant in the US and China, and amid news of the potential for fresh travel restrictions across several countries. Carbon prices continued their upwards trajectory this week, with the EU ETS up by 3.6% to average €55.32/t, and the UK ETS boosting 7.5% to average €46.64/t, finding support from a tight European gas market.

Wholesale Price Snapshot

Energy Wholesale Market Review Week Ending 6th August 2021.

Written By Graham Paul

{kind=link}